3/5/22 Prices

I’m starting to read a lot more private analyst reports pointing towards a collapse in the US housing market, not the same as the 2008 collapse but fundamentally the same net result. The volume of speculation in the US housing, financial and commodities markets at present is worrying. A couple of months of 50c currency here may not be the end of the world for the Aussie exporter though……… work with me here, all I’m reading is negativity and I’m trying to shed a ray of sunshine on this huge pile of freshly printed US dollars.

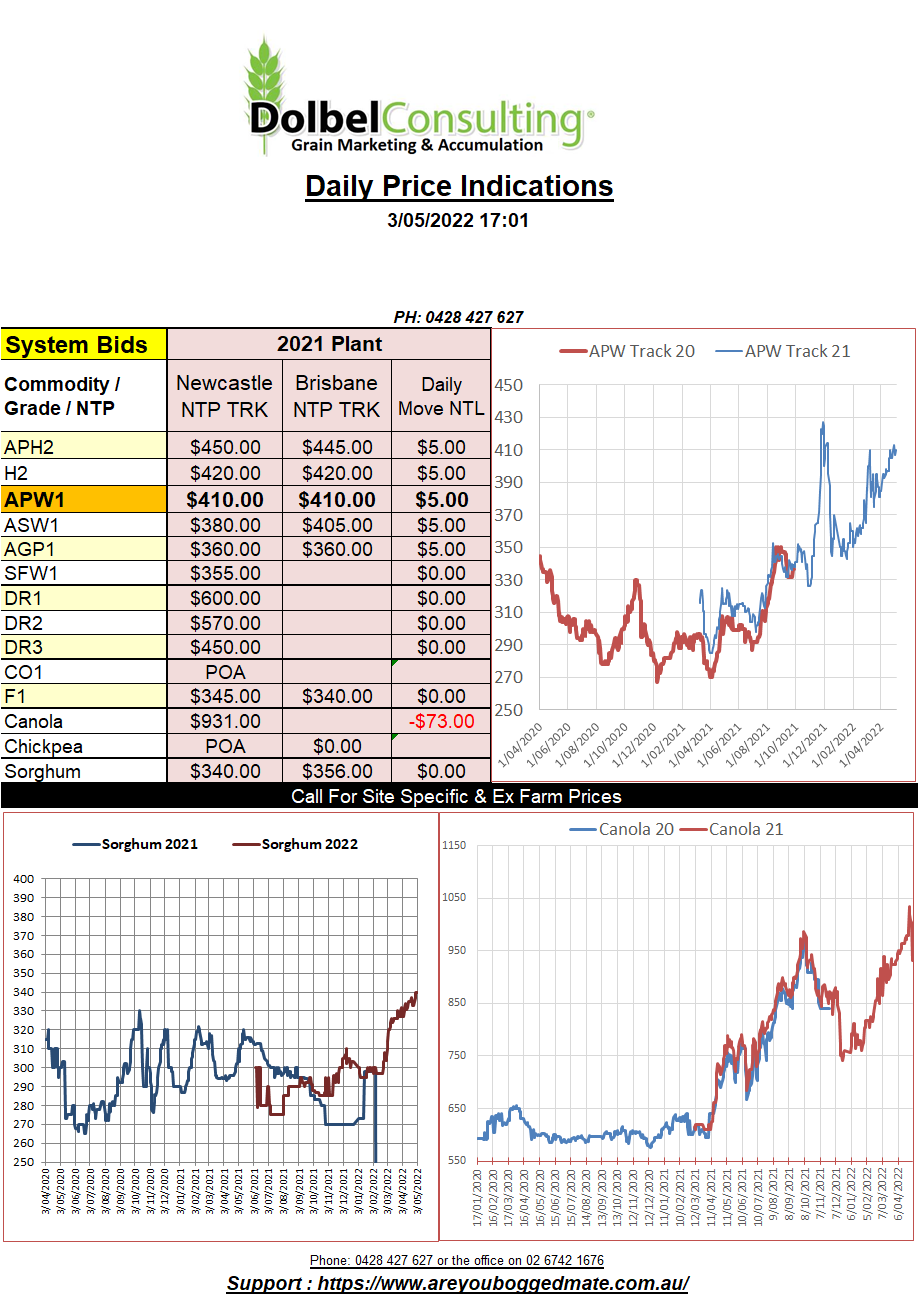

Rapeseed and canola futures were hit hard in overnight trade. Paris shed a hefty E46.25 per tonne on the August slot as May rolled off the board. In Aussie dollar terms that almost AUD$69. Winnipeg was back C$39.50 for the Jan23 slot, roughly AUD$43.50. There are a large number of influences in the global oilseed market at present. A possible decrease in Chinese imports, the increasing Indonesian palm oil stocks, the ongoing S.American soybean harvest. A sharp week on week increase in the sowing pace in US soybeans.

The more you look at the fundamentals the more you realise the bearish pressure is coming from oilseeds other than canola or rapeseed though. Weather across the Canadian prairies remains poor. Dry sown canola is quickly running out of moisture, anything that started to germinate will die without rain over the next week or two. Canola (and sunflower) production is not as bearish as the other oilseeds. This may simply be the case of fleeing speculators and spread traders though. One might think if this was the case would basis improve, good luck with that.

US corn planting was pegged at 14%, that’s well below the 5 year avg of 33%. As for winter wheat condition ratings in the US we see things remaining generally the same to possibly worse, Kansas rated at just 25% G/E and 39% P/VP. This will make those punting swaps a little nervous.